Keep pace with the rapidly evolving fintech industry by subscribing to the BIGcast Network. Get weekly insights from industry leaders John Best and Glen Sarvady, delivered straight to your preferred podcast platform. Join our community and stay informed about the latest trends shaping the credit union industry. Subscribe today and ensure you’re always ahead of the curve.

New Analysis Supports Credit Union “Everyman” Claims

Based on the size of the audience Americas Credit Unions’ economic team attracts, I’m clearly not the only one who considers their Economic Update one of the highlights of the annual Government Affairs Conference. You can hear some key takeaways from my interview with Curt Long and Dawit Kebede here, but my favorite “aha moment” is best conveyed visually.

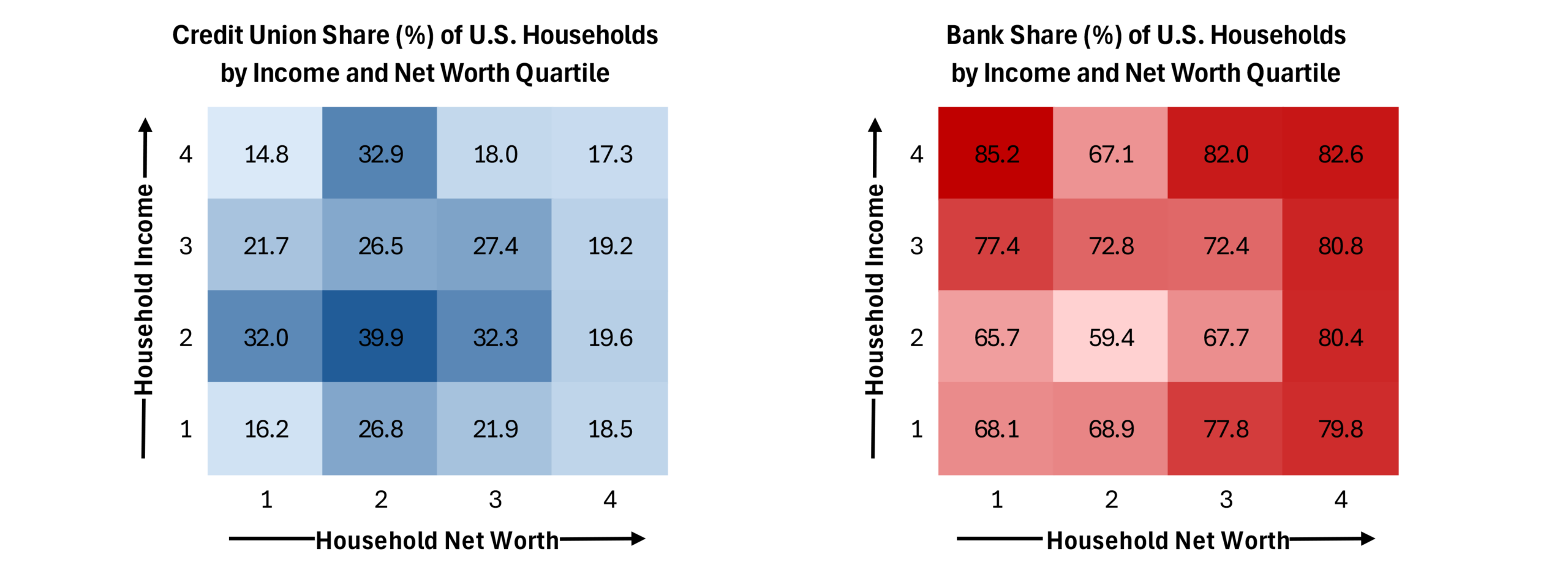

A frequent selling point is that credit unions excel at providing financial services to everyday working Americans. A new ACU analysis does an excellent job of backing up this claim. There are two distinct dimensions to affluence: a household’s annual income, and its net worth. Wealth can be found in either form- for instance, a retired couple may have modest annual income but a very solid base of net worth to provide financial security.

In order to consider both categories, ACU broke each into quartiles and created 4×4 matrices (Quartile 1 being the lowest, 4 the highest) and calculated credit unions’ market share in each of the 16 buckets. The results are striking:

Credit unions’ greatest relative strength resides with households in the second quartile of household income, i.e., below the median but above the lowest 25%. The single greatest spike in market share- just under four in ten households- exists among those in the second quartile of both annual income and net worth- which is pretty much the definition of middle class (or slightly lower). There is another somewhat surprising spike (32.9% share) among top quartile income households that have yet to amass a median level of net worth- these may be younger families with significant earning potential who have found CUs to be valuable partners in building toward their long term goals.

I find Americas Credit Unions’ analysis, which is based on Federal Reserve Survey of Consumer Finance data combined with proprietary research, to be highly enlightening and thought-provoking. It’s also heartening evidence that credit unions indeed “walk the talk.”